Research

Research

My research studies expectations, disagreement, forecasting, and the way information affects macroeconomic policy and financial markets.

Mind the Gap: Disagreement and Credible Monetary Policy

AbstractHide abstract

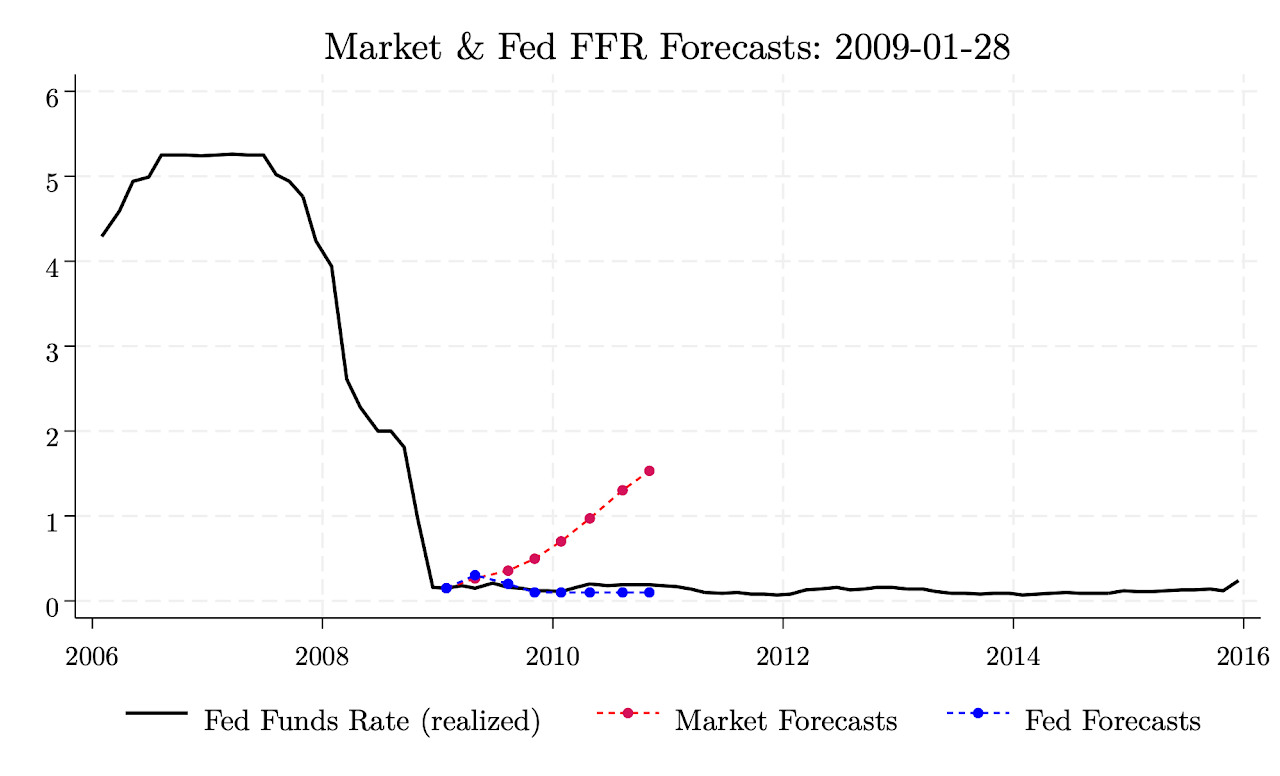

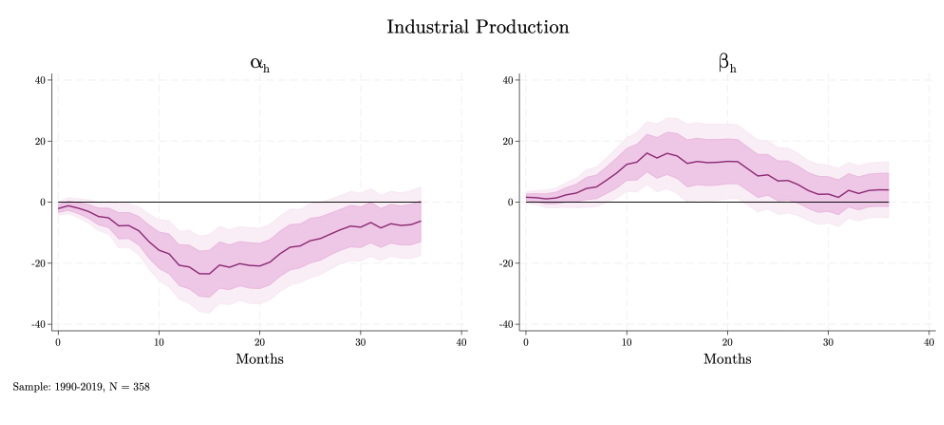

This paper studies the impact of interest rate disagreement between the Federal Reserve and financial markets on the transmission of U.S. monetary policy. First, I construct a simple real-time measure of disagreement and show that it improves short- and medium-horizon forecasts in standard macroeconomic VARs. Second, using lag-augmented local projections, I show that disagreement dampens monetary policy effectiveness, attenuating its impact on output and offering an explanation for apparent anomalies such as the “activity puzzle.” Third, I demonstrate that market expectations, as reflected in tradable asset prices, outperform Fed staff forecasts, and that information-advantage tests reveal no systematic Fed edge, challenging prevailing narratives. I show that standard New Keynesian frameworks with incomplete information contain a latent disagreement structure, which, when formalized, yields a parsimonious explanation of the documented evidence. The model generates disagreement from three distinct sources — fundamentals, policy rule, and credibility. A general state-space model identifies the importance of each and sheds light on key normative implications.

Presentations

International Research Forum on Monetary Policy (May 2026), EAYE Annual Meeting 2026 (May 2026), Federal Reserve Board (Mar 2026), Johns Hopkins University (Mar 2026), University of Surrey (Feb 2026), CEMFI, Banco de España (Jan 2026), Banca d'Italia (Jan 2026), IMIM–Rising Stars (Virtual Conference, 2025), South Cal International Macro Finance (USC, 2025), Midwest Macro Meetings (Kansas City Fed, 2025), UCSD Macro, Rady School of Management (2025).

CiteHide citation

@article{amodeo2025mind,

title={Mind the Gap: Disagreement and Credible Monetary Policy},

author={Amodeo, Francesco},

year={2025}

} High-Frequency Cross-Sectional Identification of Military News Shocks

with E. Briganti

AbstractHide abstract

This study develops a two-step procedure to identify and quantify fiscal news shocks. First, we augment a narrative identification strategy using Large Language Model searches to compile events (2001–2023) that altered the expected path of U.S. defense expenditure. Second, for each event, we estimate market-implied shifts in expected defense spending with cross-sectional regressions of contractors’ stock returns on their reliance on military revenues. We show that this approach statistically validates each event, quantifies each shock in an intuitive, model-consistent fashion, and readily generalizes to other macroeconomic contexts. Employing the estimated shocks in a shift-share analysis yields a two-year MSA-level GDP multiplier of approximately 1 for U.S. military build-ups.

Presentations

Bocconi, Bank of Canada, XXIII Bank of Italy Public Finance Workshop.

CiteHide citation

@techreport{amodeo2025high,

title={High-Frequency Cross-Sectional Identification of Military News Shocks},

author={Amodeo, Francesco and Briganti, Edoardo},

year={2025},

institution={Bank of Canada Staff Working Paper 2025-27}

} AbstractHide abstract

This study proposes a novel approach to interpreting conventional tests of the Full Information Rational Expectations (FIRE) hypothesis, based on the distinctions between forecasts and expectations. First, I argue that these two objects coincide under highly restrictive conditions that are unrealistic in the context of professional forecasting. Evidence from reduced-form analysis suggests that forecasters pursue strategic incentives when responding to surveys, contaminating their responses and making their use as measures of expectations misleading. Second, I leverage this distinction to introduce a new parsimonious model of forecast formation that is related to rational inattention and sparsity-based models of bounded rationality, but that is exempt from their complications, including the dependence on Gaussian information. The proposed framework employs a global game structure featuring public and private information, as well as the strategic behavior of forecasters, and demonstrates that strategy can explain the anomalies in Coibion and Gorodnichenko (2015)-type regressions. Finally, I exploit the model’s transparency to develop and apply a formal test that validates the strategic channel, advising caution in using surveys to elicit expectations.

Awards

- Richard A. Libby Research Award

- Best Research in Macrofinance – $10,000

Presentations

EAYE Conference (King's College, London 2025), Sailing the Macro Workshop (Ortygia, 2024), UCSD Macro Lunch Seminar Series, Rady School of Management Finance Seminar Series (San Diego 2023, 2024), NBER Behavioral Macro Bootcamp (Berkeley, 2023).

CiteHide citation

@article{amodeo2024strategic,

title={Strategic Forecasting},

author={Amodeo, Francesco},

journal={Available at SSRN 5145169},

year={2024}

} Identifying Monetary Shocks: It’s All in the (Orthogonalization) Timing

AbstractHide abstract

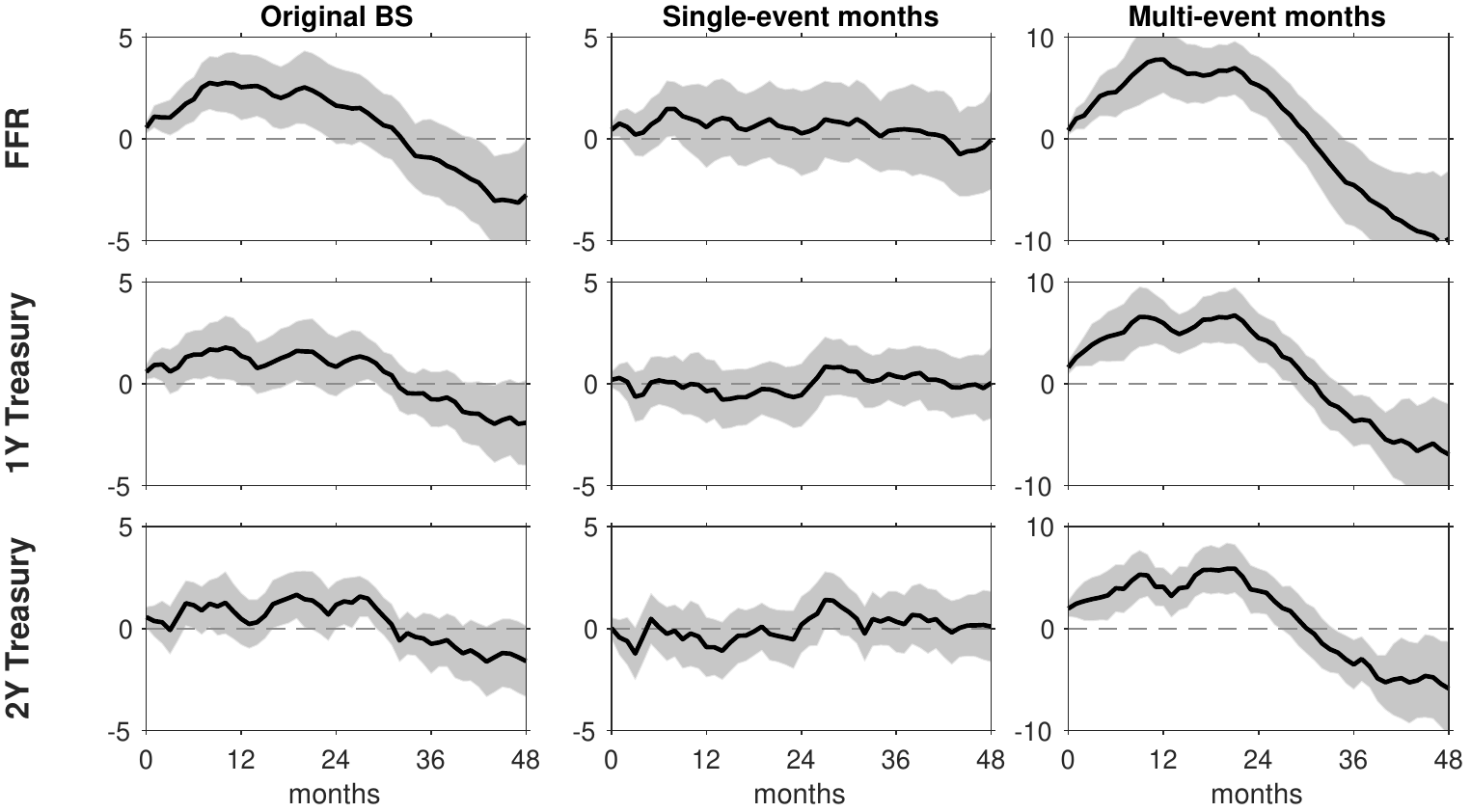

High-frequency surprises are a popular instrument for monetary policy shocks, and yet they are predictable from information already public at the time of the FOMC announcement. Orthogonalizing them against pre-announcement macro-financial predictors has become the state-of-the-art way of reinstating instrument validity. This paper shows that when surprises are aggregated to monthly, the timing of orthogonalization becomes part of the identifying design. I illustrate this in the orthogonalized monetary surprises of Bauer and Swanson (2023a): their series sums within-month surprises and purges the total using first-announcement predictors. I show that the obtained instrument retains a predictable component, therefore identifying a combination of shocks and news effects. Instead, I orthogonalize each surprise against its own pre-announcement information set and then aggregate. Under this method, first-stage strength collapses and the large macroeconomic responses reported are no longer statistically detectable. I rationalize the stark differences: the original instrument’s power is concentrated in multi-announcement months — exactly where a first-announcement purge cannot remove later-announcement information. A simple model explains the asymmetry and formalizes orthogonalization timing as part of the identification design.

CiteHide citation

@article{amodeo2026identifying,

title={Identifying Monetary Shocks: It's All in the (Orthogonalization) Timing},

author={Amodeo, Francesco},

journal={Available at SSRN 5450974},

year={2026}

} AbstractHide abstract

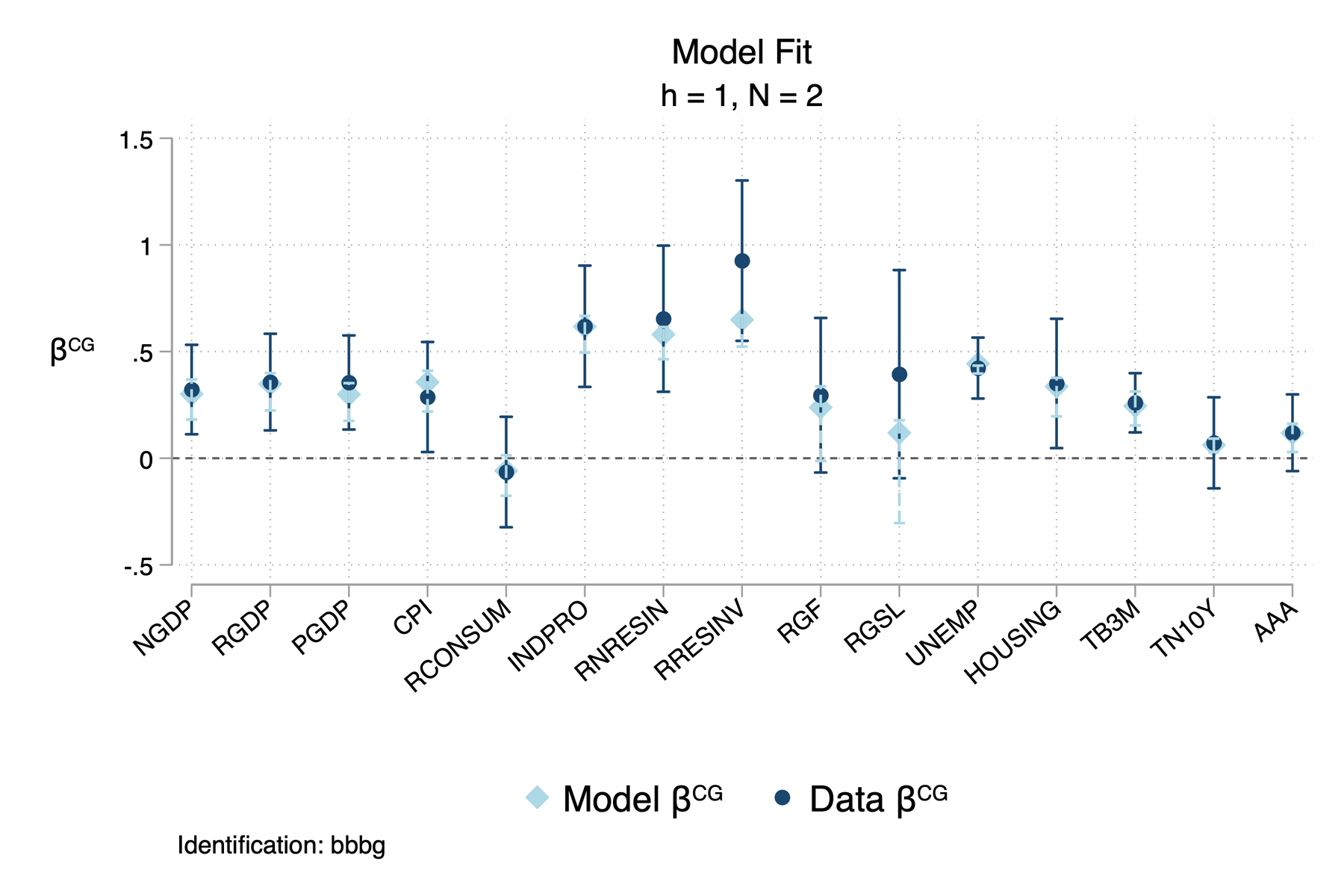

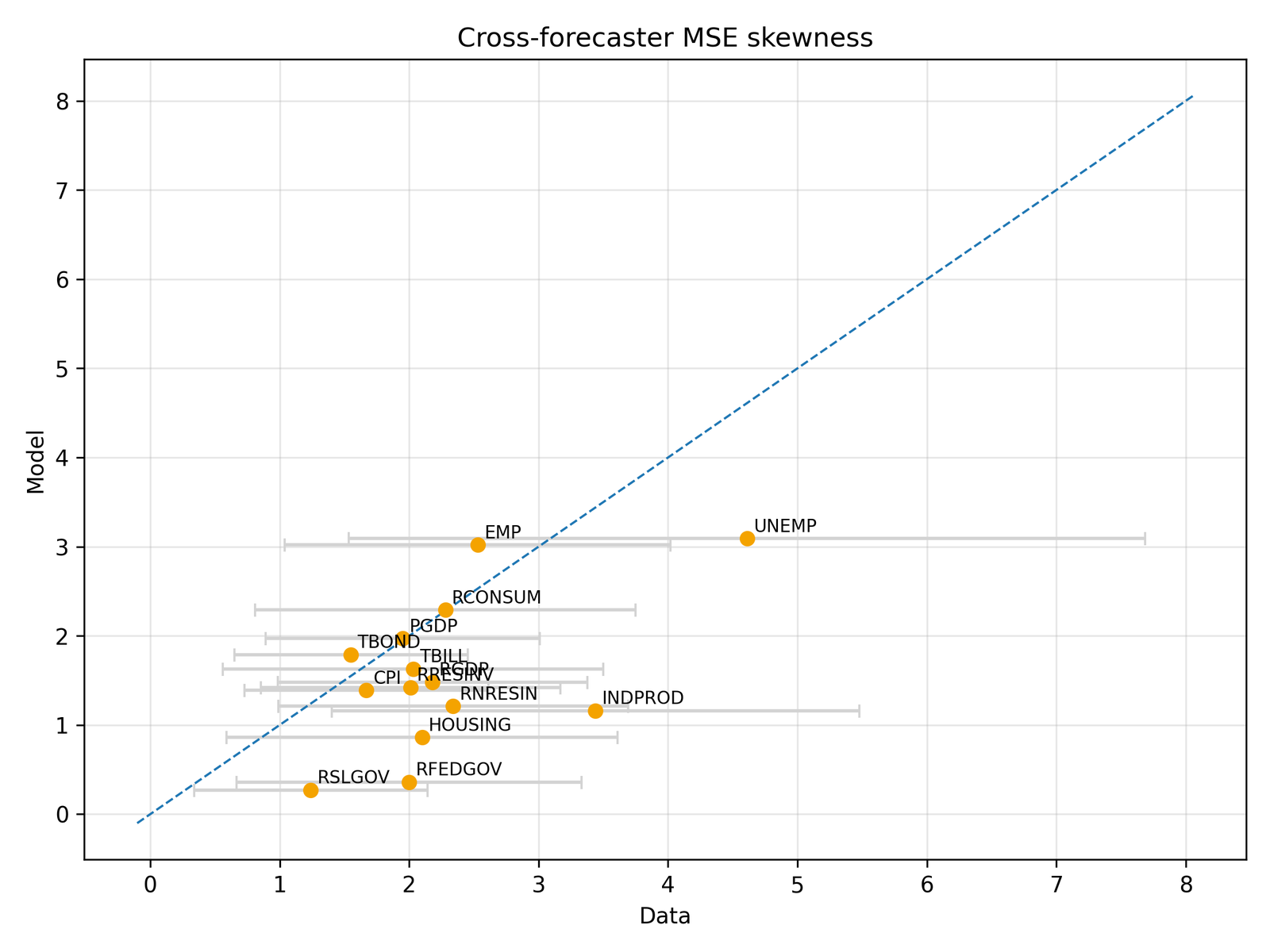

We explore two major surveys of macroeconomic forecasts to examine patterns of heterogeneity in the cross-section of forecasting performance. We identify a range of new stylized features of forecast accuracy that, we show, are robust across horizons, variables, and surveys. We argue that many of these properties cannot be accommodated by existing models of noisy information or sticky expectations. Instead, we develop a parsimonious heterogeneous-agent hybrid model that features both noisy information and sticky expectations. We calibrate the parameters of this model and demonstrate through simulations that this model comes closer to fitting the data.

AbstractHide abstract

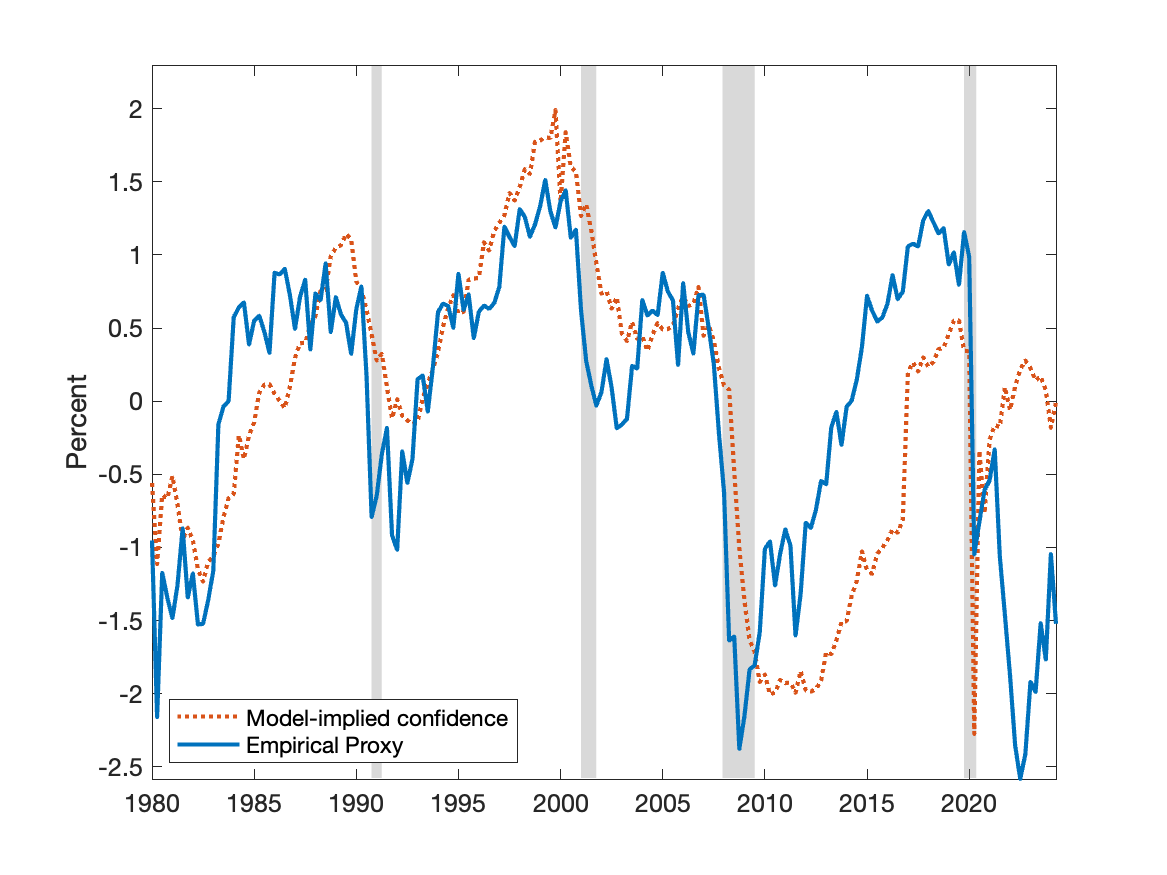

What portion of the movements in real estate prices cannot be rationalized by the most commonly imputed economic factors? How much should we care about the “animal spirits”, intended as fluctuations in agents' beliefs, when studying the origination of financial crises? The goal of this paper is to assess the role of confidence in understanding the boom-bust dynamics of credit and house prices in the United States, with a focus on the Great Financial Crisis. We identify confidence shocks in a structural VAR as exogenous innovations to the University of Michigan Sentiment Index. A positive shock to confidence increases significantly and prolongedly house prices, and accounts for almost 30% of their variance after 12 months, remaining significant after five years. We embed confidence shocks in a DSGE model with households’ heterogeneity and financial frictions. Confidence shocks are modeled as exogenous shifts in beliefs that are unrelated to current and future economic fundamentals, and that can generate waves of optimism or pessimism about current economic activity. Results from a Bayesian estimation of the model show that innovations to confidence account for half of the volatility of observed house prices. Our estimated confidence series shows a strong positive correlation with the Sentiment Index, suggesting that belief fluctuations in the model resemble empirical measures of confidence.

Presentations

UCSD Macro Lunch Seminar Series, Rady School of Management Finance Seminar Series (San Diego, 2023, 2024).

AbstractHide abstract

Economic models with input-output networks assume that firm or sector growth is driven by a combination of trade partners’ growth and idiosyncratic shocks. This assumption generates unrealistic restrictions on network weights. Allowing for correlated shocks exposes units to additional risk that captures their ability to substitute away from supply and demand shocks. I provide evidence that substitutability between trade partners is related to technological and product dispersion that is not captured by standard firm and industry definitions. I propose a production-based asset pricing model in which supply chain substitutability depends on product/technology dispersion and shock correlation driven by shared suppliers and customers. The model predicts that assets positively exposed to upstream and downstream shocks are useful hedges and earn lower average risk premia than less exposed peers. This is confirmed by estimated return spreads of -11.4% and -4.2% and a negative association with aggregate growth.

Ethics, ESG and Returns: A Behavioral Experiment

with V. Bufalari, C. Consolandi

AbstractHide abstract

This paper studies how ESG labeling influences investment behavior. In a controlled experiment, participants allocate portfolios across otherwise identical assets, some labeled as belonging to an “Ethical Index.” Investors systematically favor ESG-labeled assets, even absent financial incentives, revealing a behavioral preference for ethical framing. Both inclusion and exclusion announcements affect demand asymmetrically, with stronger reactions to ESG signals than to conventional ones. The findings demonstrate that ESG information can shift portfolio choices through non-financial motives, highlighting a behavioral channel in responsible investing. A simple model of “ethics-adjusted” mean–variance utility generates the documented demand shifts with testable empirical predictions.